When it comes time to start withdrawing the money you've spent a lifetime accumulating in your retirement portfolio, you want to ensure that you make the right decisions.

One decision the government makes for you is requiring that you withdraw at least some of your funds annually, depending on your age and the account type. This is known as a required minimum distribution, or RMD, and it must be taken from your retirement accounts (other than Roth IRAs) by December 31st each year, starting the year after you turn age 70½. (Your first RMD may be postponed until April 1st in the year after you turn age 70½.)

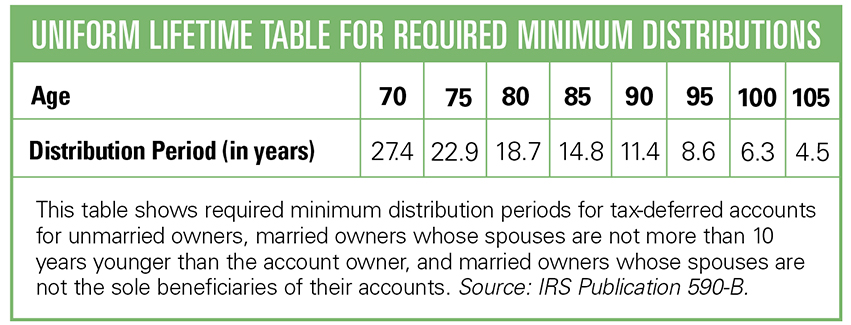

Generally, an RMD is determined using uniform life expectancy tables that take into consideration the account owner's and/or account beneficiary's age and marital status, as well as their account balance(s) as of December 31st of the year prior to the distribution year.

The exact distribution amount changes from year to year. It is calculated by dividing an account's year-end value by the distribution period determined by the Internal Revenue Service. For instance, an account holder with a $100,000 traditional IRA at age 75 would need to withdraw $4,367 ($100,000/22.9), or 4.37 percent of the total balance.

Here are some important considerations for those entering the distribution phase of their investing lives.

You can pick the account(s) you withdraw from...

If you have more than one of the same type of retirement account—such as multiple traditional IRAs—you can either take individual RMDs from each account, or aggregate your total account values and withdraw this amount from one account. As long as your total RMD value is withdrawn, you will have satisfied the IRS requirement.

…Unless they are two different types of accounts.

If you own more than one type of account, such as an IRA and an employer-sponsored plan account, you'll need to calculate your RMD for both types of accounts separately and take the proper amount from each.

You may be able to defer if you're still working.

If you are still employed at age 70½, you may be able to defer taking RMDs from your employer-sponsored plan until after you retire. You'll need to check with your employer to see if this applies to you.

The implications for failing to comply can be severe.

If you fail to take your full RMD, the IRS may assess an excise tax of up to 50 percent on the amount you should have withdrawn, and you'll have to take the distribution.

Taxes are still due upon withdrawal.

You will probably face a full or partial tax bite for your distributions, depending on whether or not your traditional IRA was funded with nondeductible contributions. Note also that the amount you are required to withdraw may bump you into a higher tax bracket.

You can donate your RMDs to charity.

If you are an IRA owner, you can contribute up to $100,000 of your IRA directly to qualified charities and have it count toward your RMD. If you've inherited an IRA, these donations are allowable as long as you are over age 70½.

Roth IRAs are exempt.

If you own a Roth IRA, you don't need to take an RMD. However, note that any distributions taken from a Roth IRA do not count toward your RMD amount, and restrictions apply to the beneficiaries of inherited Roth IRAs. Also note that the RMD rules do apply to Roth 401(k)s.

Like many tax rules, those governing minimum distributions can be complex. Don’t wait until end of year to begin calculating your RMD and withdrawing funds. iBi

Cathy S. Butler, CFP, CRPC is a financial advisor with Morgan Stanley. For more information, visit www.morganstanleyfa.com/cathy.butler.