College costs are growing at a rate faster than inflation, along with student loan debt. To help maximize every available dollar, it’s important to have an understanding of 529 plan rules and other funding options.

What Is A 529 Plan?

A 529 plan is a tax-advantaged college savings vehicle. In Illinois, there are two 529 plans: Bright Directions and Bright Start. The average fees for Bright Directions can range from 1.06 to 1.56 percent, plus an initial sales charge of 3.50 percent for A shares. In contrast, the age-based index portfolios in the Illinois Bright Start plan use Vanguard funds with average fees of 0.13 percent (fees for other Bright Start portfolios range from 0.13 to 0.41 percent). The Bright Start program can be attractive because it offers passively managed portfolios at a lower cost.

Furthermore, Illinois allows a tax deduction for contributions to a 529 plan of $10,000 per year for a single filer, or $20,000 per year for those married filing jointly. That’s a tax savings of $49.50 per $1,000 contribution, or $495 per taxpayer if $10,000 is contributed.

One strategy available to Illinois taxpayers is to use a 529 plan as a pass-through vehicle when funding college from cash flow in order to receive state tax deductions. This means you can deposit the amount (up to the deduction allowed) to pay tuition into the 529 plan, and then withdraw it the next day to pay tuition—providing you with a state tax deduction along the way.

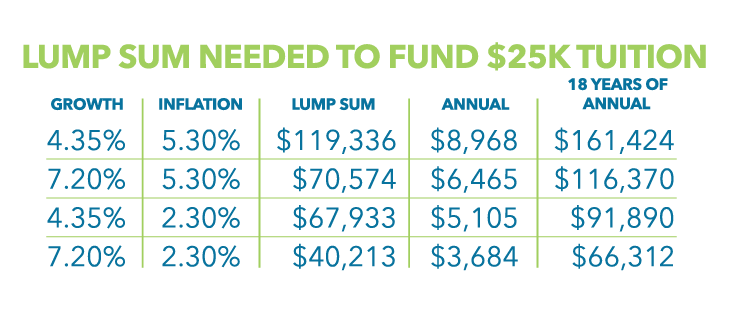

How Much Do I Need To Save?

Parents often worry about saving enough for their child’s college education. Sometimes they even worry about saving too much and what to do with the extra funds. The following chart shows the amounts needed to fund four years of college in the future, estimated at $25,000 per year, using assumptions of two different college cost inflation rates and two different portfolio growth rates.

If inflation outpaces portfolio growth, you will need to save more to have enough funds in 18 years. In contrast, if growth rate exceeds inflation, you can get by with saving less. The cost of tuition in 18 years, however, is a big unknown.

One strategy to avoid overfunding a 529 account is to fund it with up to 75 percent of the expected future cost of college. If it’s a lump sum, you may want to start by funding just 50 percent of the expected future cost upfront. Other factors to consider in determining how much to save are the number of children you have, the potential for graduate school, and any other saving and spending goals you may have.

My Child Will Not Attend College… Now What?

You can change the beneficiary of a 529 plan to any of the following: children (including foster children) and their descendants; siblings or step-siblings; parents (including step-parents); nieces and nephews; aunts and uncles; sons-in-law, daughters-in-law, fathers-in-law, mothers-in-law, brothers-in-law or sisters-in-law; your spouse or the spouse of any of the foregoing individuals; or first cousins.

Keep in mind that there may be gift tax consequences for changing a beneficiary to someone who is not a member of the current beneficiary’s family (as defined above), or who is more than 12½ years younger than the current beneficiary if not a descendant (even if a family member). If changing the beneficiary isn’t desirable, you also have the option of withdrawing the funds and paying a 10% penalty along with tax on the earnings.

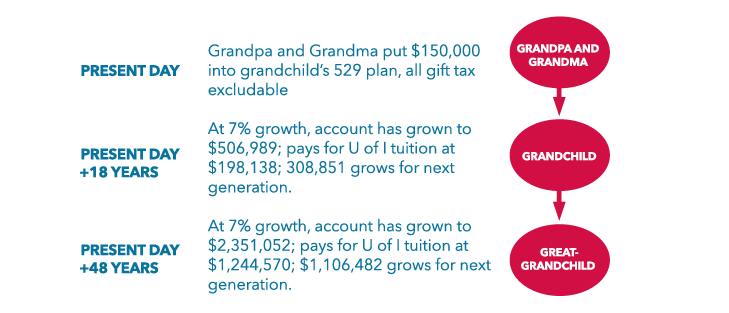

Growing For The Next Generation

As a final thought, consider the impact of allowing a 529 plan to grow for the next generation—or even the one after that. Here is an example of what to do with unused 529 plans:

A 529 plan may be a great way to set up a multi-generational college funding program! Also note that no trust or attorney is needed to set this up. (Keep in mind that in some cases gift taxes may apply, as noted above.)

College planning can be a stressful topic, but tools are available to help you gain confidence and plan for your child’s brighter future. PM

Daryl Dagit is market manager and financial advisor in the Peoria office of Savant Capital Management. He can be reached at (309) 693-0300.

- Log in to post comments