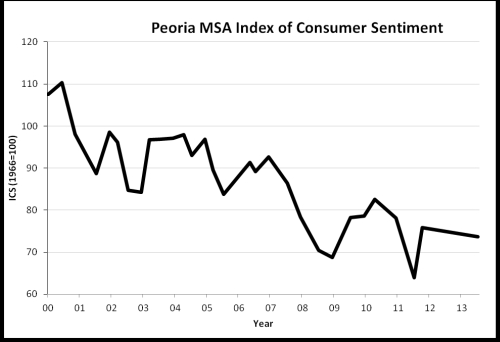

Consumer confidence in the future declined among households in the five county Peoria Metropolitan Statistical Area (MSA; Peoria, Tazewell, Woodford, Marshall, and Stark counties), reducing the Peoria MSA Index of Consumer Sentiment (ICS) to 73.7 in August-October 2013 from the 75.9 found in the previous survey of January-March 2012.

Peoria MSA surveys of consumer confidence are conducted each year by the Center for Business and Economic Research (CBER) of the Foster College of Business at Bradley University. The ICS measure used by the CBER replicates the ICS used nationally by the Institute for Social Research at the University of Michigan. The ICS is based on measures of family financial condition, expectations for future family finances, expectations for business conditions in the year ahead, business cycle expectations, and assessments of buying conditions.

Declines in confidence for the future among Peoria MSA residents were reflected in less positive expectations for the future of family finances and for the future of the economy, including increasingly negative expectations for business conditions, for unemployment and for interest rates The local findings of declining confidence in the future are consistent with declines reported nationally by the Institute for Social Research of the University of Michigan.

Although confidence for the future fell, improved assessments of current buying conditions and improved family finances were recorded among households in the Peoria MSA.

ECONOMIC EXPECTATIONS

Overall attitudes to the near term future of the economy fell, with the 41 percent with negative expectations outnumbering the 21 percent positive. Specific economic attitudes for the near term are reported below.

Future Unemployment: Attitudes about future changes in unemployment became net negative, with 34 percent (up from 18 percent previously) that expects rising unemployment in the year ahead, versus 11 percent that expects reduction in unemployment (down from 27 percent previously).

Future Interest Rates: Concerns about the potential for rising interest rates increased, with 62 percent that expects higher interest rates, up from 37 percent that expected rates to rise in the previous Peoria MSA survey of 2012. Caution about the use of credit cards was expressed by a majority (53 percent) of consumers, who stated in response to a direct question that they had reduced or even eliminated their credit card use altogether.

Future Family Finances: Families are less optimistic about their future finances than in 2012, with the 17 percent expecting improvements in their finances in the year ahead (down from 24 percent previously) only slightly above the 15 percent expecting a financial decline for the family (up from 11 percent previously).

Future Inflation: Consumer expectations are for modest inflation, with an average 2.9 percent inflation expected in the year ahead, up from the 2.2 percent rate projected by area residents in our last survey.

Buying Homes: The perception of a favorable market for buying homes declined, with 66 percent (down from 76 percent previously) reporting favorable buying conditions for homes. When asked the reason for their attitudes to home buying, the appeal of low interest rates on mortgages was cited most frequently (41 percent); the appeal of low prices was mentioned by 20 percent (down from 51% in the previous survey); a good supply of homes for sale was noted by 13 percent. Eighteen percent cited negative assessments of the economy as the reason for their attitudes to home buying.

Business Cycle Expectations: Long term expectations for the economy were increasingly negative, with the 62 percent worried about a recession in the five years ahead up from 56 percent in the previous survey, and close to the 65 percent concerned about a recession in the long term that was recorded two years ago.

CURRENT CONDITIONS MEASURES

Family Financial Condition: Feelings about family finances improved from the previous survey, and become net positive, with the 38 percent stating that they are “better off” (up from 30 percent previously), now outnumbering the 31 percent feeling “worse off;” (The 31 percent “worse off” is little changed from the 30 percent of 2012.)

Increased income was mentioned by 27 percent of families as a factor affecting their finances (up from 22 percent previously), while decreased income was mentioned by 24 percent of families as affecting their family finances (little changed from 2012). Fourteen percent singled out better income from their present jobs (working more hours and/or higher pay rate) as improving their finances, outnumbering the 11 percent that mentioned reduced income from present jobs (working fewer hours and/or lower pay rate); 11 percent complained of the impact of higher prices as a factor producing change in their family finances.

Buying Conditions: Increasingly positive attitudes for buying major household durable goods were found with a majority (54 percent) that states that it is a “good time” to buy major household durable goods, up from 46 percent favorable previously.

REVIEW AND OUTLOOK

The impact on the Peoria MSA ICS of improved family finances and buying conditions in the August-October survey was outweighed by declining expectations for the future, declines similar to those reported nationally by the Institute for Social Research of the University of Michigan.

The decline in the Peoria MSA ICS for August-October 2013 signals reduced willingness by area families to engage in discretionary purchases in the coming months.

BACKGROUND

Investigators at the Institute for Social Research of the University of Michigan originated the ICS as a national measure over 60 years ago.

The Center for Business and Economic Research (CBER) at Bradley University began local household sample surveys of consumer confidence during the severe national recession of 1981-82, when an ICS of 53.6 was found. The area ICS achieved expansionary (i.e., over 90) levels in late 1987. The ICS fell to 71.7 in 1990. Boosted briefly in April 1991 by post Gulf War euphoria, the Index fell back to 70.7 later that year, and remained low through October of 1992. The area Index for November 1992 rose 14 points following President Clinton's election in November 1992.

The local ICS continued at favorable levels for the next eight years, peaking at 110 in the fall of 2000. The ICS fell 12 points in early 2001, and

continued to decline until it was below 90 by the time of the terrorist attacks of September 11, 2001. Solidarity following the attacks pushed the ICS upward, but later 2002 measurements revealed the resumption of the earlier downward trend that continued until early 2003.

The local ICS recovered in the context of the national expansion later in the last decade, and reached 92.7 in Spring 2007. The local ICS declined in the context of the national recession of December 2007- June 2009), and had fallen to its cyclical low (below 70) by the first quarter of 2009.

METHOD: The surveys of Peoria MSA economic attitudes are performed by Dr. Bernard Goitein, Director of Survey Research at Bradley University's Foster College of Business with funding provided by the Foster College of Business.

The survey results are based on telephone interviews with households in the Peoria MSA performed during the evenings of August-October 2013.

A random sample of 601 listings was used, based on area telephone directories and a commercially available phone number database. Interviewers attempted to contact the designated respondent in each of the homes, using up to six contact attempts during varied days and times of day in the survey period.

Using these procedures, 458 (76 percent) of the sampled respondents were reached and asked to participate. Interviews were successfully performed with 188 households, for a 41 percent cooperation rate.

The chances are about seven in ten that if every residence listed in area directories and the commercially available phone number database had been approached using these questionnaire administration procedures, the percentages found to the survey questions would have differed from those observed in this sample by no more than four percentage points in either direction.

Peoria MSA Consumer Sentiment Report 61 © Bradley University